Le prossime mosse del governo e dell’opposizione dopo l’approvazione del Recovery fund. Gli scenari nel report di luglio della School of Government della Luiss

Italian politics has always been an arcane subject. A handful of specialists and enthusiasts love to talk of its Machiavellian intricacies for hours on end, but most people, especially north oftheAlps, not only do not understand it, butsee no reason why they should bother to understand it. Today there are at least three reasons why they should. First, in Italy the crisis of the political establishment that is now evident in many advanced democracies began a quarter century ago. This means that the country is further down the road of the democratic malaise – it is a laboratory and a bellwether. Second, Italy is the first country from within the historical core of the European community to be governed by anti-establishment parties. Third, its politics represent the greatest threat to the stability, or possibly even the existence, of the common European currency. Founded in 2010 in a University that has a very strong international vocation, the Luiss School of Government aims to facilitate the connection between Italy and the world outside of it. It aims to prepare the future Italian public elite for the complexities of an ever more integrated planet, and to provide first-class education to non-Italian students in Italy’s capitalcity. SoG professors have often helped non-Italian journalists and newspaper readers understand Italian politics. Thus, it seems only natural to me that the Luiss SoG should offer amonthly report on Italy that provides an interpretation of the country’s recent political events, and makes an educated guess about what happens next (Giovanni Orsina Director, Luiss School of Government).

Politics

The political path forward for Giuseppe Conte is getting narrower. If the States General for the economy have helped the government get through the summer, many political and economic problems will arise for Conte in the autumn,when itwill be necessary to decide on the 2021 budget. In Parliament, the signs are clear, there is an increasingly clear convergence between a faction of the 5 Star Movement and the League, on both fiscal policy and the relationship with Europe. A scenario that depends on two factors: first the weakness of the Five-Star leadership and the lack of trust of part of the Movement in the moderate transformation imposed by Grillo and Giuseppe Conte and by the alliance with the PD; second the need for the League leader Salvini to free himself from opposition. The breaking point in the government majority might be the Five Star Movement. Not only due to the increasingly evident division into differentf actions, but due to what the Movement's parliamentarians will soon have to face: irrelevance at the territorial level (they have no hope of governing the Regions); further confirmation of the drop in consensusin the regional elections in October; a very likely "blood, sweat and tears” budget law owing to the worsening GDP estimates; the probable need for the governmentto resort to the ESM, which will be the death knell for the Eurosceptic, anti-establishment posture of the Movement (IL RECOVERY FUND VISTO DA MADRID E DA BERLINO).

At that point, the dissatisfied parliamentarians will make a simple calculation, elections remain unlikely both due to uncertainties on the health front and due to the relative majoritiesin Parliament and, in any case, in the case of both early or distant elections, the 2018 resultremains unrepeatable for the 5Star Movement. In other words, many know that they have no hope of beingre-elected and, atthe same time, that the legislature is unlikely to end before 2022. Consequently, the Five Star parliamentarians could begin to look for a new political home, where it would be possible to be reelected in the next general election. In this context, Salvini has played his cards, aware both ofthe League's attraction forthe grillini (Five Star members) and of the numbers in the Senate that are not very reassuring for the majority (now the majority there is +5 seats). Moreover, the League’s strategy is to ensure that this majority does not choose the next President of the Republic. And everyone knows, as a note of uneasiness in Matteo Renzi's most recent interviews reveals, that in this legislature there has already been another majority (League and Five Star Movement). A problem for the centre-left, which aims to activate the ESM and bring its own preferred candidate to the Quirinale (or, possibly, to reconfirmMattarella). Berlusconi is back in town.

The tycoon is deploying his strategy, positioning Forza Italia between the majority and the opposition. There are rumorsin Rome around Berlusconi’s ideas and many analysts Monthly Report on Italy No. 5 July 2020 5 of 15 bet on Forza Italia joining the majority, particularly if the Five Star Movement splits in the next few months. However, in all likelihood, Berlusconi’s strategy is more subtle. He knows that his party cannot breakwith itsright-wing allies Salvini and Meloni and that, consequently, Forza Italia cannot join the majority. But, in the meantime, Berlusconi’s party is still part of the EPP in Brussels, and he does notwant to disappointhis Europeanfellows. In this scenario, Forza Italia might help the majority occasionally, perhaps voting infavour ofthe ESM programme, where the Government would not have enough votes in Parliament owing to the defection of the radical factions of the Five Star Movement. This position would be profitable for Forza Italia: the tycoon would regain political centrality, he could be the swing vote for the election of the new President of the Republic, but without renouncing the right-wing alliance at local and national level.

Di Maio’s game. Until a few weeks ago, Di Maio was considered a second-division leader, exhausted by the political leadership of the Five Star Movement and overshadowed by the Prime Minister. However, in the Five Starleadership void, the Ministerfor ForeignAffairsstill hassome cardsto play. He still has some grasp over the Five Star parliamentary groups and he could influence the opinion of dozens ofMPs disappointed by the government. In his position, Di Maio has every interest in breaking the link between the 5 Star Movement and the Prime Minister, because control of the party, or at least part of it, is the only asset he has for his political future. Giuseppe Conte is a problem for Di Maio, in terms of both leadership and alliances.While Di Maio is arguing for an independent Movement, open to multiple alliances, the Prime Ministeris working for tighter cooperation with the Democratic Party at national and local level. If this scenario came true, Conte would become the next natural leader of the Five Star Movement. However, Di Maio’s potential to veto can not be ignored: with a weak executive and a precarious majority, controlling a portion of the Five Star Movement means having the capacity to notably influence the government. In recent weeks, Di Maio met the former President of the ECB Mario Draghi. A sign that the Five Star Movement’s former frontman is not excluding a new government without Giuseppe Conte as a future option.

The results of the EUCO’s recovery package. Prime Minister Conte has obtained mixed results from the European Council meeting, which established the European stimulus package for the recovery of the economy after the pandemic. In the initial phase, Conte aimed to obtain more grants than loans, but the final agreement reformulated the compromise among member States, increasing loans at the expense of grants. Moreover, the Italian government was looking for a lower level of conditionality on reform plans, but the main European tool, the Recovery Fund, will have enhanced conditionalities and governance: it binds every country to respect European semester recommendations; it introduces a "Super emergency brake" mechanism, which allows a single member-State to block aid tranches to another Member-state by bringing the case to the European Council,which will decide by consensus (unanimity) on the reformplans of the country underscrutiny.

Now Conte has to convince his majority, and even more the Italian citizens, that Italy is no more a “special observed”in Bruxelles and that the government has negotiated successfully. Italy should get around 80 billion grants and 120 billion loans, a resultwhich is not the best for the government but is not too far from the initial target, either. In the end, considering the difficulties of the European negotiations, if these numbers are confirmed, Conte will have achieved a remarkable political result. Another positive achievement for Conte isthe possibility to have animmediate accessto the European funds, anticipating them already in the next budget law. During the negotiations, the Prime Minister Monthly Report on Italy No. 5 July 2020 6 of 15 was criticized by the media and the opposition because Italy was the only country that had not presented reform plans. Nowfor Conte the time has come to design priorities, policies and reforms to spend the European aids. Most of his political ability will be tested in the next months: he should convince parties in the majority to avoid clientelistic and unproductive spending and he should gain credibility with both the EU and financial markets. It will be no easy task for the Prime Minister, considering the divisions within the majority and the slowness in embracing structural reforms showed by the executive until this moment. But in political terms, if properly handled, the European agreement might act as a propellent or, at least, as a stabilizer for Conte 2.

leggi anche

Il Recovery fund visto da Madrid

Scenario

The ESM watershed. The triggering of the ESM (European Stability Mechanism) programme, in this scenario, has a fundamental role at a political rather than financial level. The government has still not announced its decision on the use of the ESM, but the PD is pushing to join the programme and to get as much as possible in terms of money fromallthe European tools. The Five Star are against the use of the ESM, because the fear a further imposition of conditionality over Italian politics. Salvini and Meloni are preparing a political campaign in case the government will decide to benefit of the ESM loans.

If Palazzo Chigi accepts the ESM, it risks playing into Salvini's hands and creating the division betweenthe Five Starministers and the dissatisfiedmembers of Parliament-with the real danger that the majoritywill collapse. At that point,with a split in the Movement and even if Conte obtained Forza Italia'ssupport on the ESM, this majority would no longer exist. As a consequence, the political forces would have to find a solution to the political crisis and the Prime Minister would be the first to risk his job.Onthe contrary,ifConte refused the ESM, a similarly difficult scenario would have to be taken into account: the dissatisfaction of the PD and Italia Viva with the Prime Minister would increase, and Conte would become a scapegoat for all the socio-economic problems. He would be perceived as a compromised leader, a prisoner of his populist origins. Reducing the amount of political friction between Rome and Bruxelleswas one of the main reasons why the second Conte government was born in the Summer of 2019. The Prime Minister has remained at Palazzo Chigi also to help the Five Star Movement mollify its euro-skepticism. A failure in managing this process will imply a loss of credibility and trust in the Prime Minister at European level. In other words, if this majority collapses, itwould be difficult for Conte to maintain his position.

What could happen in the case of a political crisis occurring next autumn? There are two possible scenarios of crisis, although the persistence of the Conte 2 today remains the most probable option. In the first scenario, a new majority is formed, composed by a portion of the Five StarMovement, PD, Italia Viva and Forza Italia. The Five Star Movement dumps its radical faction, the crisis starts, Berlusconi joins the majority and a new government is created. In this case, the Prime Minister could be a technical figure, a guarantor of the political equilibrium. This solution isthe most likely, but also the weakest option in political terms. An agreement to muddling through the legislature and to further align the Italian majority with that in Europe. The second solution is a Grosse Koalition scenario: a new government supported by allthe politicalforces, except forsomeminor groups.This case implies a convergence of the centre-right parties (Forza Italia, Lega, Fratelli d’Italia) to form a coalition with Monthly Report on Italy No. 5 July 2020 7 of 15 the PD, Renzi and (part of) the Five Star Movement. It would be an extraordinary solution given an extraordinary situation ofsocio-economic malaise. In this case, the most plausible option to be prime minister would be Mario Draghi, the most prestigious name in the Italian political parterre. A consequence of this agreement would imply the need to find a new geometry forthe election of the next President of the Republic in 2022, because all the political forces would be involved in the majority. However, today we consider this scenario as only a residual option. It is not likely that Salvini and Meloni will take the responsibility of joining a government to agree policies and reforms with PD and the Five Star Movement. Moreover,the two right-wing leaders would have to accept a deal with the EU on fiscal rules and tools, such as the recovery fund and the ESM, and their conditions. A Grosse Koalition government would be a sort of Monti 2 scenario, but national-populist political leaders are nowmore aware of howcostly supporting a technocratic government can be.

Then, there would be the third option of a snap election. We cannot exclude it completely, the parties are increasingly divided and political agreement among themmight be poorly legitimized and barely productive in term ofreforms. However, today both for healthcare and political and financial reasons (the budget law) itseems a less plausible scenario compared to the othertwo options.

leggi anche

Il Recovery Fund visto da Berlino

Forecasts

Probability of snap elections: Elections within 2020: 5% Elections within Q1 2021: 25% Elections after 2022: 70%. An early election in 2020 is very implausible at this point. A snap election in 2021 is not likely, but not impossible if the majority collapses. By July 2021 the constitutional “white semester” starts, which forbids general elections in the six months before the parliamentary election of the new President of the Republic, which will occur in Q1 2022. For these reasons, itseems very likely that the legislature will arrive at least to 2022. But under this scenario, there is no guarantee that the government (and the majority) will not change. The economic and social indicators are signalling that autumn might be tougher than expected in Palazzo Chigi. Italy is performing worse in its economic recovery than the other EU member-States. The Prime Minister will have to face a new budget law under the strict surveillance of Brussels: externally imposed (and probably unpopular) policies and tax increases will probably be unavoidable. Atthat point, there will be a stress test for the majority: if it does not pass, a new alliance among parties in Parliamentwill have to be found. Alternatively, should such an agreement prove impossible, it will have to return to the polls between autumn 2020 and spring 2021. Our baseline scenario remains that Conte 2 will stay in place. However, due to the instability within the parties and theweaknesses of the majority, we cannot completely exclude apolitical crisis between autumn 2020 and spring 2021.

Mapping risk

There are three majorr isks at this moment concerning the Italian political system: A too soft pro-European approach. The main problem for the structural reforms requested by the EU Commission is the weakness of the majority. Conte 2 was born to align Italy to the EU Parliament majority and to implement the political reforms agreed in Brussels. However, the composition of the government cannot ensure accomplishment of the programme. The Five Star Movement is still defending its anti-establishment positions in many policy areas (infrastructure, pensions, subsidies) and the PD is not proposing developmental (education, labour) and pro-business policies, but the defence of the welfare system and the promotion of State capitalism. Renzi’s party has not grown in the electoral polls and its capacity to influence governmental action is reduced. The main risk is that this pro-European majority, although it may not try to test or break European fiscal rules, will prove incapable of achieving any structural reform on pensions, welfare and the public sector. An immobility that could trigger opposite political reactions, unfavourable to Brussels-based institutions and pro-European partiesin the long term.

The shallow institutionalization of the Five Star Movement. The most remarkable sign of this political weakness is the illusion that the Five Star Movement could be institutionalized, or made more moderate and reformist. There is still a wide section of Five Star voters and representatives who do not accept the process of moderation and institutionalization. Evidence of this approach is provided by Di Maio’s political line, based on a tiring battle with Conte and the PD on every policy in order to defend the Five Star Movement’s original identity. The continuous compromises are not producing sound reforms and, in the meantime, they are not making the Five StarMovement anymore reasonable. In this scenario, the possibility of a crisis inthe current majority remains quite high, particularly ifthe government has to deliver a tough budget lawin the next fewmonths.

The return of the Entrepreneurial State. In the lastweek, the government decided to use CDP, the Italian sovereign fund, to become the majority shareholder in Autostrade per l’Italia. The State istaking the place of Benetton family to manage the Italian highway network, a decision which, coupled with the involvement of the State in Alitalia, has marked the return of the government as entrepreneur. Was it a wise decision? The choice is not without risk. The governmentis using citizens’s avings to strengthen its intervention in the Italian economy. But the Italian State is heavily indebted and any failures in business management of the newly nationalised companies would be paid for by the Italian tax payers. Moreover, the decision for more direct action by the government in some economic sectors might worry the most important industrial families, who might feelless protected byConte 2 and consider themselves at the mercy of the Italian state.

Public opinion trends: Polls

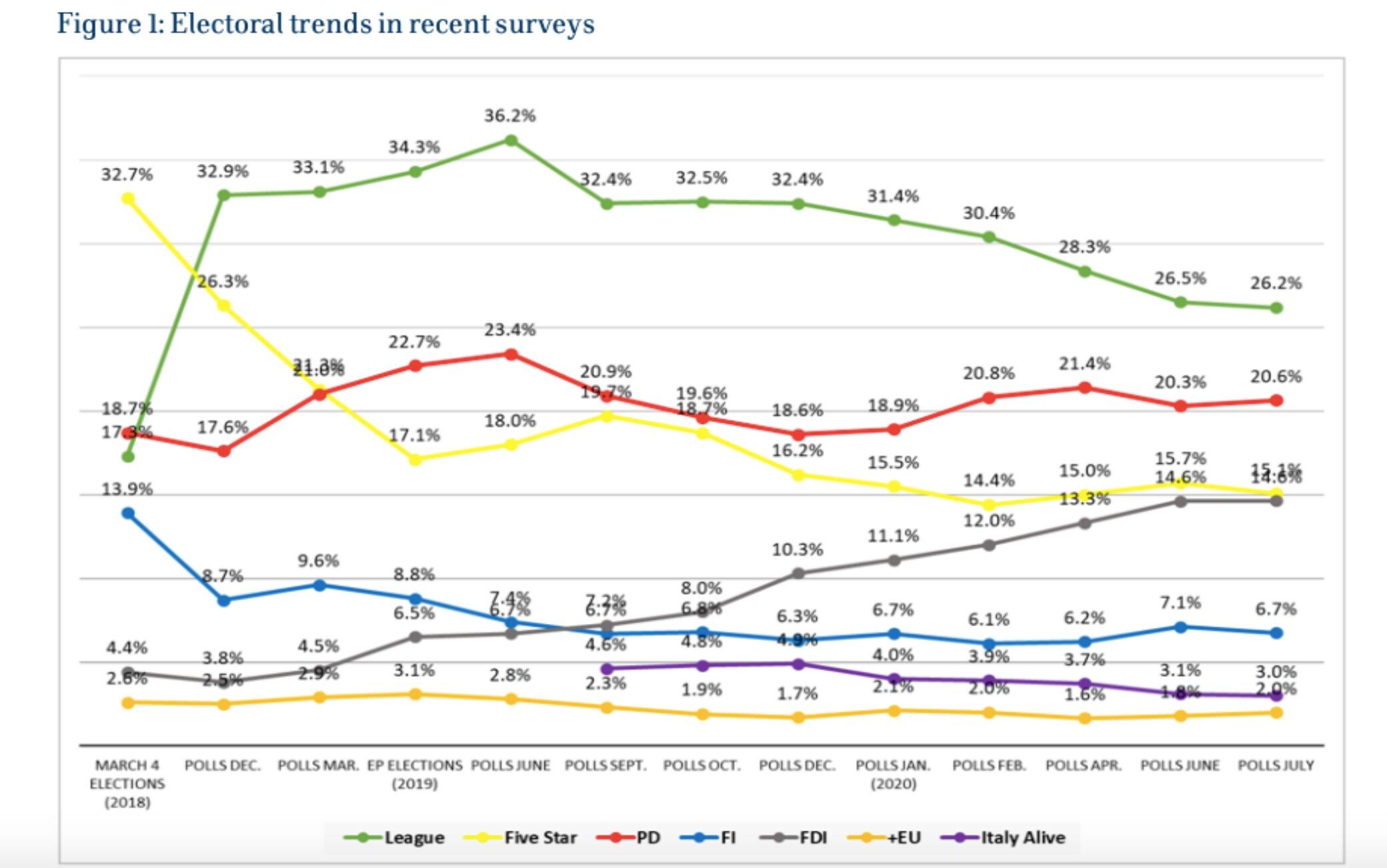

The slow electoral decline of the League continues (Figure 1). In July Matteo Salvini's party recorded a further drop of 0.3 percentage points compared to mid-June, falling from 26.5% to 26.2%. On the contrary, the Democratic Party (PD) moved from 20.3% in June to 20.6% in July. The electoral gap between the League and the main centre-left opponent is thus further narrowing, now at 5.6 percentage points, a distance that could be easily bridged in the next few months. If in the centre-right camp the League has been falling for months now, Giorgia Meloni's (FdI) party has been growing steadily since the 2018 political elections.However, betweenJune and July the party remained substantially stable at14.6%, but at only 0.6 percentage points from the Five Star Movement (M5S), whose electoral performance in turn dropped by 0.6 percentage points in July compared to the previous month. A slight negative decrease is also recorded for Go Italy (FI), which moved from 7.1% to 6.7%. Electoral performances ofItalyAlive (IV) andMore Europe have remained insteadstable aroundrespectively 3% and 2%.

Overall ,the government area collects 41.6% of the votes, a substantially identical percentage compared to mid-June (41.5%). The electoral performance of the centre-right, on the other hand, fell slightly: in June the coalition got 48.2% of the votes, in July this percentage dropped to 47.6%. Overall, the gap between the parties in government and the centre-right political parties narrowed from 6.7 percentage points to 6 percentage points between June and July. In other words, the stability of FdI's performance, together with the drop of the League and FI, has had a negative impact on the overall performance of the centre-right. It should be noted, however, that the negative trend of the electoral performance of the centre-right did not produce a corresponding electoral expansion of the centre-left area (which has in factremained stable). In other words, the dispersion of the centre-right votesseemsto have flowed towards minorforces, currently outside the governmental area.

Regional elections

After the regional elections of January 26 in Emilia-Romagna (which reconfirmed the incumbent centre-left candidate Stefano Bonaccini) and in Calabria (where the centre-right candidate Jole Santelli was elected), six regions with an ordinary statute (Veneto, Liguria, Tuscany , Marche, Campania, Puglia) and a region with a special statute (Valle d'Aosta) will hold regional elections on September 20-21. Of the 6 regions with an ordinary statute, 2 are currently administered by the centre right, i.e. Liguria (governed by Giovanni Toti) andVeneto (governed by Luca Zaia). The other 4 regions are instead led by the centre-left. With the exclusion of Tuscany and Marche, incumbent candidates will attempt re-election in all the 6 regions. And, according to the polls of the last few days, the incumbents, inmost cases, are in the lead.

In at least 2 of the 6 regions with ordinary statutes, electoral results seem obvious already today. In Veneto ,the president ofthe region Luca Zaia (League) has always enjoyed widespread support among his fellow citizens. And this appreciation has increased in the context of the coronavirus health emergency. Furthermore, his success in this situation is projecting him outside the borders of his region, even placing himself as a potential internal rival for Matteo Salvini. A rival who in the next regional elections in Veneto is very likely to have a resounding success.

In Campania as well, the coronavirus seems to have benefited the incumbent governor Vincenzo De Luca.Before the pandemic,the results ofthe regional election in Campania were far from obvious. The pandemic explosion has instead raised the level of support for De Luca, to the point that the unitary candidate of the centre-right, Stefano Caldoro, does not seem able to threaten the re-election of the incumbent governor. According to the Winpoll-Arcadia poll estimates (last week of June), 65.4% of Campania'svoters are now intentioned to vote for De Luca, against 21.9% and 10.9% of those who would vote respectively for the centre-right candidate Stefano Caldoro and the M5S candidate Valeria Ciarambino. Even taking into account the large number of abstentions and the significant portion of the electorate whose choice isstill uncertain, thisis clearly an extraordinary result that demonstrates the personalsuccess of De Luca.

In Liguria and Tuscany, the outcome of the elections is only slightly more uncertain. In Liguria, the centre-right supports the incumbent president Giovanni Toti, who enjoys moderate appreciation among the voters of the region. The parties currently in national government (especially the PD and the M5S), have not yet managed to agree on a common candidacy to oppose the centre-right. Liguria isthe only regionwhere anagreement betweenthe two main government partners still seems possible today. However, although negotiations are underway, the outcome of these negotiationsis uncertain, to the benefit of the centre-right coalition,which isfor nowin the lead.

In Tuscany, a traditional leftist stronghold, the incumbent governor Enrico Rossi will not run in the elections for the centre-left. In his place there will be Eugenio Giani, challenged by the League candidate Susanna Ceccardi. For the M5S, the candidate for the presidency of the regionwill be Irene Galletti. Although Salvini's League has managed to impose its candidate onthe centre-right allies, and although the political forces currently in government (PD and M5S) have not managed to form an alliance at the local level, the polls seem to give the centre-left the lead. If the data were confirmed, the political orientation of the regional administration would be confirmed.

The scenario in Puglia and Marche is more complex and uncertain, compared to the other regions. In Puglia, the candidacy of the incumbent presidentMichele Emiliano (PD) is notsupported either by the M5S or byMatteoRenzi's party (ItalyAlive),which will run with their own independent candidates. In Puglia, therefore, the political parties in national government appear even more fragmented than elsewhere. The centre-right forces have instead reached a joint agreement in support of the sole candidacy of Raffaele Fitto (FI). The fragmentation of governing parties clearly weakens Emiliano's candidacy and indirectly strengthens the centre-right front, which, according to the latest polls, is today the favourite towin the election in the region.

Marche (together with Tuscany) is the other region where the incumbent will not run in the regional election. In fact, the incumbent centre-left governor Luca Ceriscioli was not selected by the PD as a candidate forthe regional presidency. Themayor of Senigallia, Maurizio Mangialardi, will run instead for the centre-left. The centre-right supports Francesco Acquaroli (FdI). As in the case of Puglia, Marche could move from the centre-left to the centre-right. The lack of agreement on a common candidacy between the two main forces of the national government undermines the possibility forthe candidates of both the PD (Mangialardi) and the M5S (Mercorelli) to be competitive against the united front of the centre-right. In other words, the inability to negotiate and find convergence at local level between the PDand the M5S could hand overthe region to the centre-right. Monthly Report on Italy No. 5 July 2020 12 of 15.

In summary, the government experience at national level of the PD and M5S does not seem to have had positive effects at the local and regional level. Political parties currently in government will run the regional elections on their own, thus showing a concrete difficulty in translating the experience of the national governmentto the local level. Except for sudden twists and turns, the situation is not likely to change much in the coming months and if the scenario just discussed above were confirmed by the vote in September, the consequences both at national and local level could be very significant. At the local level, there would be a clear rebalancing of power relations between the centre-left and centreright. If the forecasts were confirmed, the centre-right would be able to keep the two regions it has administered in the last five years (Veneto and Liguria) and would snatch two regions (Puglia and Marche) from the centre-left. From a total of 4 out of 6 regions administered by the centre-left, we would therefore move to a total of 2 (Tuscany and Campania) out of 6, with a reversal of the starting situation. At the national level, the implications of such a scenario would be at least two. First of all, the lack of local agreement between the PD and the M5S would clearly reveal the fragility of a government experience that seems to be the result of circumstance; in fact, the main partnersin government seem to be unable to mutate the coalition at the national level into a more solid and structural alliance. In general, this would raise serious doubts about the possibility of forming a coherent progressive alliance in the near future, including both the PD and the M5S, to oppose the centre-right coalition. Secondly, the eventual defeat ofthe centre-leftwould force the PDto rearticulate a long-term strategy, which would allow the party to become competitive not only at local, but also at national level.

Economic Scenario

On July 7, the EU Commission (EC) presented the updates for GDP forecasts in the Summer 2020 Economic Forecast, where they highlighted an even deeper recession and wider divergences, with the reason being that the economic impact of the lockdown has been more severe than initially thought. The latest forecasts show that the Italian economy will contract the most among all Member States, with GDP growth of -11.2% for the current year. It is important to note that the change in the forecasts should not be linked with a worsening of the current or future situation, but is merely due to an underestimated recession for the first quarter of the year. Nonetheless, the EC forecasts a rebound of 6.1%in ItalianGDP growth for 2021.

The Italian Cabinet, with the aim of removing some bureaucratic obstacles to support the country’s recovery, approved on July 7 the “Semplificazione” Law Decree introducing urgent measures structured around four main objectives that aim for the simplification of several areas of interest, for the digital transformation of the public administration as well as for the orientation towards a green economy. The first aims at simplifying public procurement contracts to stimulate investments in the infrastructure and servicessectors. The second focuses on the simplification of the currently complex and articulated procedural process and the introduction of new incentives regarding responsibilities for public officials. The third point concerns simplification measures supporting the digital transformation of the public administration, and lastly some measures aimed at easing processes for businesses aswell as oriented towardsthe necessary green economy transformation.

Recent talk of a cut in direct and indirect taxes had fuelled doubts about the country’s commitment to economic reform linked with the Next Generation EU, in amoment when its EuropeanUnionallies are Monthly Report on Italy No. 5 July 2020 13 of 15 trying to persuade sceptics, represented by the ‘frugal four’ (Austria, Denmark, Netherlands and Sweden), that the country can be trusted with a massive stimulus package. A tax cut might even be implemented but only with the requirement that it be temporary, in this way households might be induced to increase consumption today with the idea that prices will be higher in the future. The problem with a permanent tax cut concerns the sustainability of this measure; in fact, lower tax revenuesfor the government meansit is necessary to find othersourcesto maintain the current level of public spending.However, given the large amount of money coming fromtheNextGeneration EU, a drop in tax revenues might be sustainable in the short term, but complications arise when the EU funds are over but the tax and spending structure implies increasing the former or decreasing the latter, given that an additional increase in public debt for tax cutsis not on the table. Fortunately, the EC approval required to use grants/loans of the Next Generation EU will mean that these funds cannot be used for a permanent tax cut.

From the ‘Estates General’ talks with social partners on ways to find a sustainable recovery for the country, there emerged the guidelines for the National Reform Programme (NRP). The plan for the three-year period 2021-2023 delineated by the Minister for Economic Affairs and Finance, Roberto Gualtieri, points at stimulating an economic recovery and fostering long-term economic growth by acting on innovation,sustainability,social inclusion and territorial cohesion, in the new environment characterised by the pandemic.Inparticular,to pursue these objects ,the Governmenthas highlighted the following interventions: the relaunch of public investments,with a minimum target of 3%of GDP, together with an increase in spending on education and R&D and then stimulating private investments, aiming at strengthening the competitiveness of the economy with reforms that allow for more equity, social inclusion and environmental sustainability.

The relevance of the NRP is crucial as it will include the Recovery and Resilience Plan, a necessary document for Member States where they formulate a set of investment and reform priorities that are needed to access the new Recovery and Resilience Facility, the bulk of the funding from Next Generation EU, thatwill be assessed by a committee composed of Member States’representatives and then approved by the EC. The Planrequiresthe document to be integrated with the related investment packages to be financed under the facility through instalments depending on progress made and on the basis of pre-defined benchmarks, with the interruption of instalments should the State fail to complywiththe investment and/or reform targets set out in the NRP. It is important to note that, based on the EC’s proposal, the Recovery and Resilience Facility will be accessible to all Member States, but support will be concentrated onthe parts of the Union most affected andwhere resilience needs are the greatest.

Based on the ECB proposal, funds raised for the Next Generation EU financed by long-term EU borrowing will be repaid from the end of the Multiannual Financial Framework (MFF), 2027, and by 2058 at the latest. The EC recovery plan plays a crucial role when some national public finances are undersevere strain, in fact, this will make it possible to leverage the revamped long-term EU budget, allowing the EC to raise funding on financial markets to spread the financing costs over time, so that Member Stateswill not have to make significant additional contributions to the EUbudget during the 2021-2027 period. Nevertheless, the final political agreement on several building blocks of the final version of the economic recovery package is hard to obtain, with “frugal” governments which are Monthly Report on Italy No. 5 July 2020 14 of 15 critical ofthe proposed size ofthe fund, pushing for cutsto the EC’s proposal of €750 bn, and itsmixture of grants and loans, asthey oppose a recovery that would provide grant funding.

On July 10, the President of the European Council, Charles Michel, proposed to reduce the size of the EU long-term budget from €1.1 tn to €1.074 tn, but kept the EC’s €750 bn proposal for the recovery instrument unchanged. Concerning the funding, Michel considers it essential to include grants and not just loansin the recovery package in orderto avoid overburdening the Member Stateswith higher levels of debt and to avoid higher fragmentation and disparities within the Single Market, with Member States that are highly indebted and others that have more fiscal space to employ for the recovery. He proposed 70% of the recovery fund to be allocated in the next two years, 2021 and 2022, with the rest committed for 2023 and distributed by 2026. The difference with the original ECproposal is that the Council recommended to bring forward by two years the repayment of the debt from the fund, in 2026, and to introduce EU revenues from three areas: plastic waste, carbon adjustment mechanism and the digital levy. In this regard, on July 17 the next European Council meeting will gather the leaders of the 27 EU Member States in Brussels to discuss the EU’s next seven-year budget, with particular emphasis on the economic recovery package proposalswhere disagreements are not over yet.

In this crisisthe European Central Bank (ECB) has been able to cross a number of previousred linesto allow Member States to forget about debt sustainability issues for now. In fact, the ECB by implementing itstemporary Pandemic Emergency Purchase Plan of €750 bn for asset purchases, later on increased by €600 bn to a total of €1.35 tn, has hugely stabilised sovereign bond yields. Nevertheless, debt sustainability remains an issue for whenever the ECB will be forced to sell those bonds in the secondary market, that will not be before the end of 2022, with yields that will again be extremely exposed to investors’ decisions. It is clearly not a problem of the near future, given the current inflation and the open-ended horizon of the ECB’s Asset Purchase Programme (APP), but when the inflation outlook changes the ECB’s policies will need to adjust as well, exposing highly indebted countries at severe risk of default on their debt. Hence, as public debt is soaring due to extraordinary national measures and sovereign yields are temporarily kept low by ECB programmes, it is imperative to include in the national and EUplan forthe economic recovery a strategy to reduce the huge burden of public debt on national governments, thus avoiding undermining Europe’s future prosperity and resilience and allowing more flexibility for national fiscal policies to react to future challenges.

A very controversial political argument concernsthe use of the Pandemic Crisis Support, based on its Enhanced Conditions Credit Line (ECCL), that might provide Italy with up to €36 bn in near-zero interest loansfor expenses on direct and indirect health sector costs. The main political arguments of the Five Star Movement plus the League and Brothers of Italy firmly refuse the fund’s activation, dubbing it a trap of Brussels’making and implying that accepting itwould impairItalian sovereignty. In addition, the two major right-wing opposition parties suggest issuing national bonds, with yields around 1.3%, to cover healthcare expenses. It should be clear that this is a mere political debate without any logic whatsoever; in fact, the spread between the interestrate using national bonds and the rates using the ESMcreditline is clearly positive and the only conditionality isto spend thismoney ondirect and indirec the althcare expenses. Thus, should we need to reinforce the healthcare system, also taking into consideration a possible major second Covid-19 wave in the autumn, Italy should undoubtedly Monthly Report on Italy No. 5 July 2020 15 of 15 make use of the Pandemic Crisis Support, and in thisway save billions in interest payments over a 10- year horizon. We have already wasted too much time and too many resources due to political caprice, nowisthe time for diligent action.

)

)

)